Crypto vs. TradFi

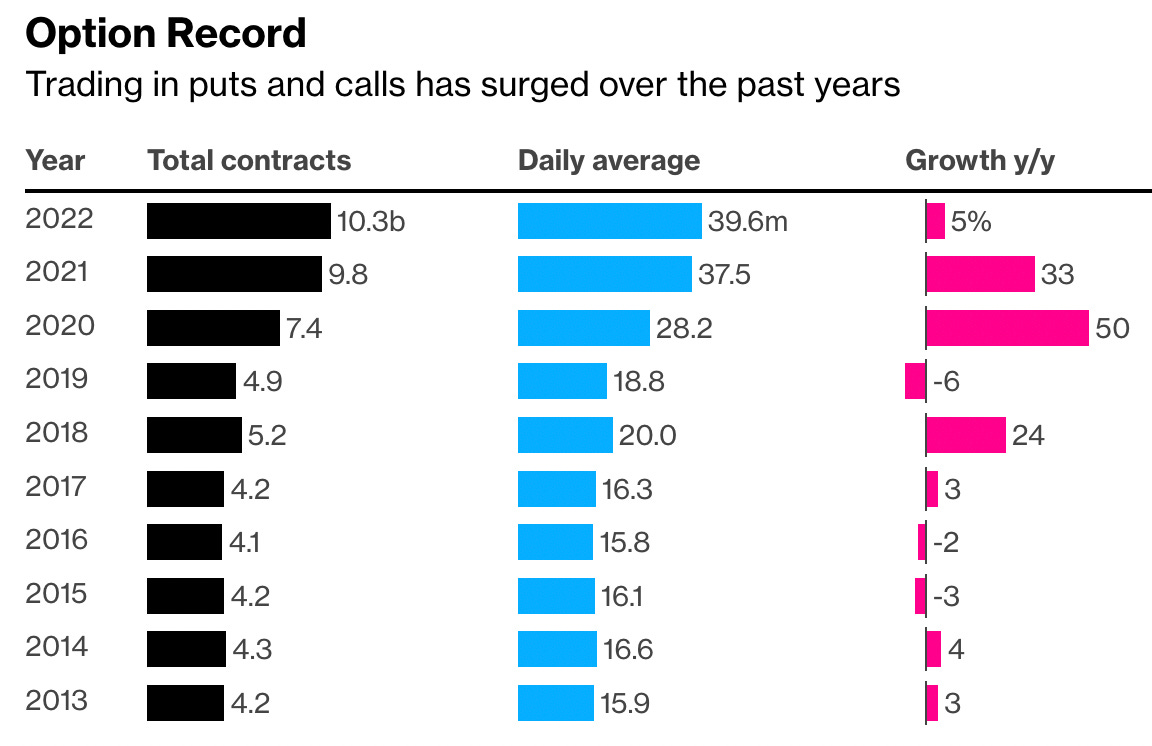

You probably know that options are a big deal in TradFi. In 2021, for the first time ever, the notional value of daily options trading exceeded spot trading in the U.S., and the number of equity and index option contracts traded on all Opra exchanges has now grown three years in a row.

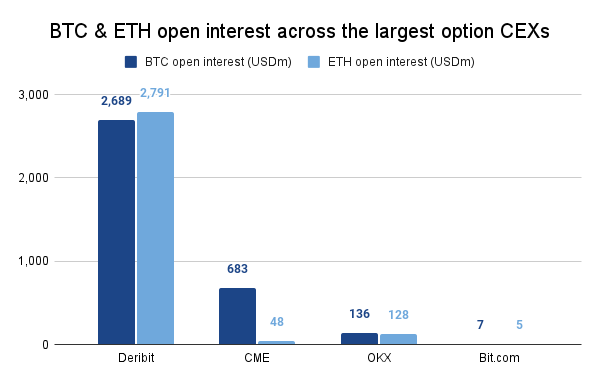

Usage of options in crypto pales in comparison to TradFi. In December 2022, the average daily notional options volume for BTC and ETH was ~USD 430m on CEXs, which only represented ~2% of the average daily spot volume traded for the two tokens. Deribit is a clear market leader for option trading across CEXs, with OI for BTC & ETH currently at ~USD 5.5bn, which translates to a ~85% CEX market share. Compared to CEXs, on-chain option volume is minimal. For example, Ribbon, one of the largest option protocols, transacted ~USD 205m of notional volume on Ethereum in December 2022, and the current OI for all assets on Lyra, one of the more established option AMMs, is ~USD 5m.

In 2021, a strong narrative around on-chain options was forming, but since the beginning of the bear market in H1 2022, the hype has somewhat dampened. No DeFi options venue has managed to garner significant and long-lasting usage, with TVL across notable protocols (Dopex, Hegic, Ribbon, Lyra, Premia, Opyn) having decreased by ~81% during 2022. According to DefiLlama, the total TVL across option protocols is currently ~USD 195m, of which ~65% is accounted for by the four largest protocols (Opyn, Ribbon, Dopex, Lyra).

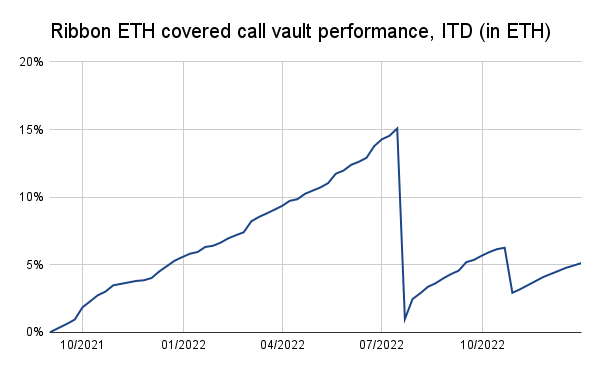

Protocols have historically bootstrapped liquidity by boosting LP returns through emissions. As emissions decrease, capital flows elsewhere since LPs face high opportunity costs and returns become unsatisfactory, worsened by the fact that first-generation on-chain option solutions seldom offer hedging with respect to the underlying assets. For example, LPs for Ribbon’s automated ETH covered call strategy experienced a significant drawdown when the price of ETH rallied in the middle of July 2022.

All of that being said, DeFi options have recently resurfaced as a trending topic with the introduction of several new on-chain mechanisms designed to mitigate problems that the space has historically faced. Crypto options will inevitably attain similar adoption as TradFi options, and as protocols are continuously improving and building new solutions, on-chain options will start capturing market share from CEXs.

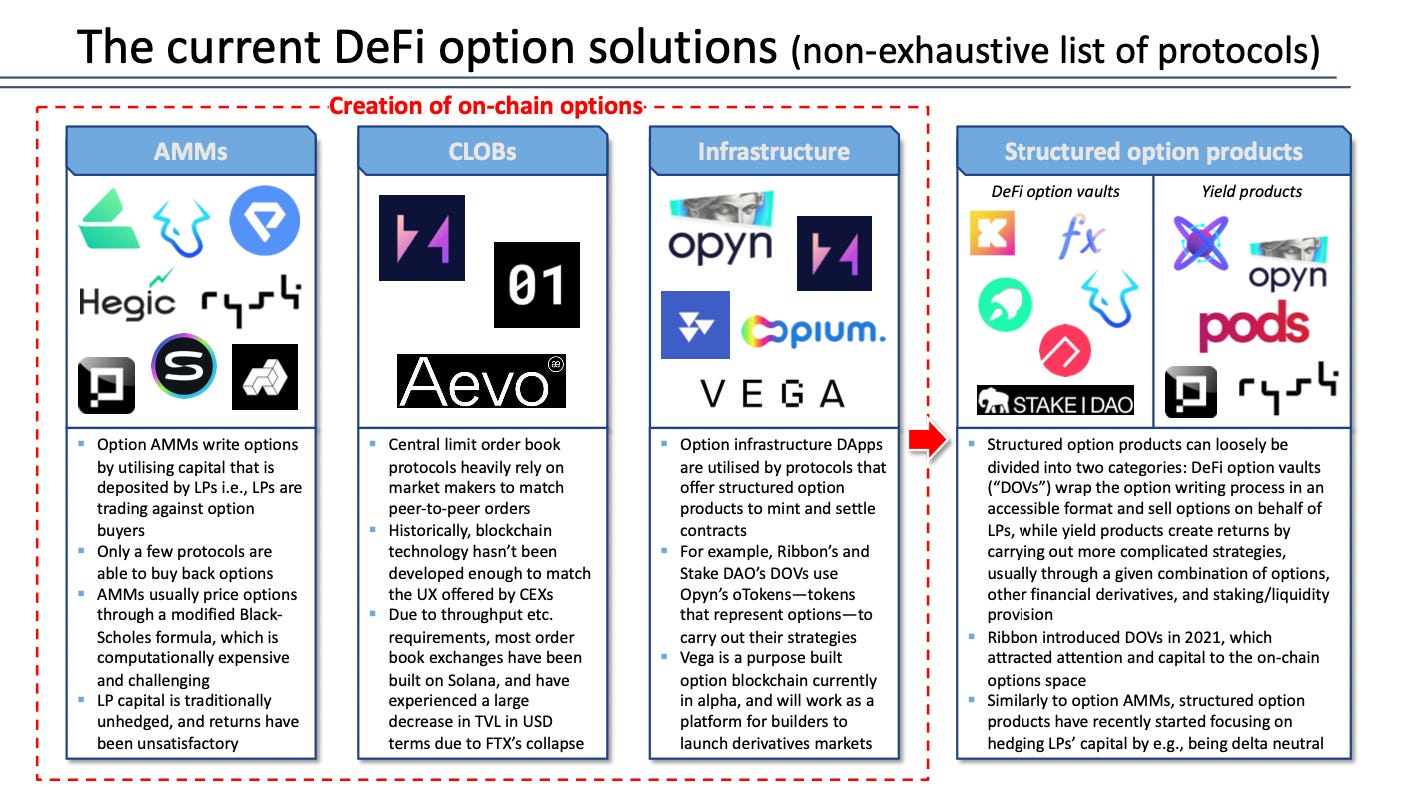

Overview of the current DeFi options space

The current on-chain options landscape can loosely be divided into four groups: automated market makers (“AMMs”), central limit order books (“CLOBs”), infrastructure, and structured option products.

CLOB-based designs are quite straightforward to understand and can be implemented in two ways: 1) on-chain, where order matching and trade settlement both occur on a blockchain; or 2) hybrid, where order matching occurs off-chain and trade settlement on-chain. CLOB protocols offer a similar options trading product as CEXs, but the latency and throughput limitations of current blockchain technology have resulted in a worse UX than what CeFi provides. The limitations have also restricted market makers from providing liquidity, and designing a safe liquidation engine has been challenging. Because on-chain CLOBs require cheap and fast execution, they have historically been built on Solana but with the rise of new L2 solutions and application-specific blockchains, CLOBs will start expanding to other ecosystems and improve on the aforementioned problems.

Option AMMs require LPs who deposit capital into pools that price options through a modified Black-Scholes formula, with LPs taking the opposite position to on-chain traders. Typically, AMMs are restricted from buying back options, and options are often sold at the money or near the money, resulting in larger premiums earned at the expense of more frequent drawdowns.

Option infrastructure widely comprises solutions for minting and settling contracts. This enables other option projects to build their own mechanisms on top of the infrastructure providers, which eases the development process. For example, by depositing collateral to Opyn, a partner protocol can mint oTokens, which are option contracts represented by ERC-20 tokens.

Structured option product protocols deploy LP capital, usually relying on one of the three above-mentioned categories to mint/access/settle on-chain options, which enables them to focus on yield-generating strategies. This category consists of DeFi options vaults (“DOVs”) and yield products.

DOVs function by wrapping the option writing process in an accessible and user-friendly format. Although DOVs are simple to understand and use, they are too inflexible for sophisticated traders. The vaults only underwrite options that have a weekly expiry date and are deep OTM. LPs earn a premium from off-chain market makers that buy these options and in turn hedge their positions by selling similar, short-dated options.

Yield products comprise protocols that aren’t restricted to underwriting options and instead carry out more elaborate strategies by utilising a vast array of options, other financial derivatives, and staking/lending/liquidity provision opportunities. They usually create distinctive payoff profiles and implement mechanisms to protect LPs’ capital through e.g., delta hedging or clever protocol design.

Headwinds faced by current solutions

It’s clear that a vast amount of option-specific DeFi technology and mechanisms have been developed. However, some implementations utilised today still exhibit unsolved problems in one way or another. Issues such as inefficient pricing, unsatisfactory and unclear LP returns, a limited range of maturity dates and strike prices across a small set of underlying assets, a lack of hedging instruments, and poor UX have prevented the space from growing.

Comparing TVLs across CLOB, AMM, and structured product protocols, it seems that the first group has struggled the most. The on-chain performance limitations have been a noticeable disadvantage compared CEXs and thus, most traders and market makers haven’t been incentivised to migrate on-chain. Nevertheless, the UX offered by on-chain CLOBs will most likely improve in the near-term as institutional-grade infrastructure such as wallets and the performance of blockchains develop.

By examining the payoff profiles of automated option selling strategies, it’s easy to see why the popularity of DOVs has decreased over time. For instance, when the market is in a strong uptrend, a vault that sells covered calls will significantly underperform a strategy of simply holding the spot asset because when the strike price is considerably exceeded, the yield received from selling call options is much smaller than the returns from holding the underlying. On the other hand, in a bear market, the option premiums easily become smaller than the value lost as the underlying decreases in price. Simply put, option sellers are exposed to unlimited downside in exchange for restricted upside, which is similar to a gambler utilising the Martingale betting system.

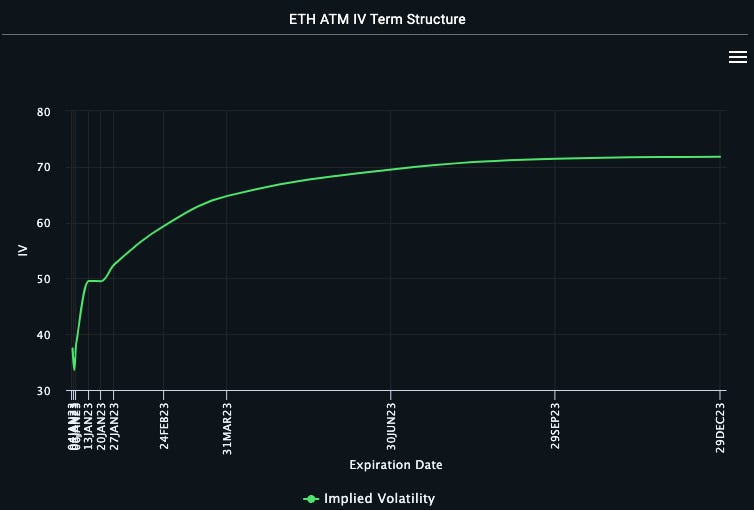

Interestingly, it’s likely that the current term structure of implied volatility is steep because of DOVs. This is because market makers that buy options from DOVs hedge their positions by specifically selling short-dated options. Furthermore, since most DOVs utilise the same weekly auction times, market participants have started pushing implied volatility lower in anticipation. As traders know that heavy selling will occur, the yield that DOV users receive has decreased.

DOVs also create misaligned incentives between off-chain market makers and vault depositors. Market makers try to purchase volatility as cheaply as possible from the vaults, while depositors want strategies that outperform the market on a risk-adjusted basis. Vaults don’t have a secondary market for offloading inventory and are therefore constrained to selling to the highest bidding market makers. Efficient price discovery is absent since there is a limited number of buyers, which leaves options underpriced.

As the saying goes—there are no free lunches. This is especially true for most option AMM LPs as they are exposed to toxic flow and unhedged positions. Takers are able to price options precisely and are constantly analysing when and where to deploy capital, while makers provide constant liquidity, which, coupled with the fact that viable option pricing by AMMs is still in development, leaves LPs vulnerable for arbitrage. Whereas makers in a CLOB-based system dynamically reprice their quotes as they implement new information about the true price, AMM LPs rely on correctly calibrated pricing functions encoded into smart contracts. Moreover, because traditional AMMs collateralise options with the underlying asset while not utilising any hedging strategies, LPs typically accumulate a high degree of exposure to the underlying and consequently, payoffs are correlated with the spot price. In comparison, conventional market makers always hedge their positions in order to create consistent profits. In other words, LPs are exposed to liabilities without adequate compensation.

From a trader’s perspective, AMMs offer a limited set of strike prices and expiry dates, which restricts the extent to which AMM options can be utilised by investors to express their view of the market or as a risk management tool. Furthermore, as most AMMs don’t allow traders to short overpriced options, price discovery becomes more inefficient.

Improvements have been made

In 2022, protocols started implementing solutions to tackle the inefficiencies discussed above. AMMs were arguably improved the most, receiving a vast array of upgrades to create more strikes and expiries. Lyra, an options AMM, is currently one of the only protocols that enables traders to both long and short options with pooled liquidity, and also allows LPs to deposit and withdraw capital at any time. This is quite unique since in general, LP funds are locked for the duration of an AMM’s epoch to ensure that risk associated with outstanding liabilities is fairly distributed.

For an AMM to underwrite options and buy them back, it has to be hedged. This is perhaps the most difficult technical implementation within option protocols, as the pool has to both dynamically calculate risk for its LPs while pricing options accordingly, and find ways to hedge its exposure through spot or futures products. Nevertheless, hedging of AMM LPs’ capital has become more widely adapted, where a protocol usually creates a position that is delta neutral. Designs still require some further development because these protocols have to charge high taker fees for LPs to reliably make money since hedging a position can become expensive. It’s important to note that delta hedging doesn’t fully eliminate risk, but it refines LP payoffs such that they derive from an AMM’s core business—market making for implied volatility and capturing spreads. Comparing the performance of Lyra’s sETH LPs across its v1 and Avalon versions, the former not having been delta hedged while the latter is, reveals that delta hedging can create a noticeable improvement. v1 LPs made an annualised return of ~(29%) during Nov 11, 2021 — Jun 17, 2022, while Avalon LPs have enjoyed an annualised return of ~8% during Jun 25, 2022 — Jan 2, 2023. Nevertheless, it’s important to note that the comparison isn’t quite like for like because of the market drawdown in H1 2022.

Protocols such as Dopex, Hegic, and Premia have tried to circumvent the delta exposure problem by splitting liquidity pools into call and put vaults, which gives users more control over the options they underwrite. However, this solution feels notably weaker than outright hedging because it offloads the continuous, capital-intensive work to end-users and fragments liquidity.

Rysk Finance is building an innovative options AMM called the Dynamic Hedging Vault (“DHV”). The AMM will be able to buy and sell options to all market participants, while interacting with other financial products to generate market-neutral yield for LPs. The DHV will price options based on an incentivisation model, where prices are cheaper or more expensive depending on the pool’s delta exposure and utilisation. The sale/purchase of options will be incentivised such that it brings the DHV’s delta exposure closer to 0. If a desired delta position can’t be attained through selling/buying options, the AMM can buy spot assets on Uniswap and perpetual futures from Rage Trade. When fully released, one of the DHV’s biggest advantages will be the ability to quote options across a broad range of strikes and expiries, increasing the liquidity of long-dated options.

In addition to hedging, focus has shifted towards improving collateralisation and capital efficiency. While conventional market makers employ a variety of hedging instruments to limit capital inefficiency, and on-chain CLOB protocols have implemented partial collateralisation and cross margining, any such mechanisms have been widely absent from option AMM and structured option protocols. The problem with full collateralisation is that it limits notional open interest to the value locked in a protocol and thus, capital efficiency is bounded. Protocols including Dopex and Lyra have started experimenting with under-collateralised solutions, the former offering Atlantics and the latter partially collateralised short positions.

Lyra’s partially collateralised short positions allow traders to sell 4–5x as many options with a given amount of capital. Naturally, this introduces the risk of liquidations, but enables the AMM to reach an equilibrium price more efficiently and has likely helped the protocol to balance the ratio of long and short positions. Before partial collateralisation became available, long positions comprised ~70% of the cumulative notional open interest on the platform. Following the introduction of partial collateralisation, the split of cumulative notional open interest between long and short positions is split ~50-50. A more balanced basket of options in the AMM leads to lower vega risk, resulting in lower utilisation fees, and ultimately to better prices for traders.

Dopex’s Atlantic options are an interesting play on collateralisation. The option purchaser has the right to borrow the collateral that the option writer deposits, with the option writer earning a funding fee for lending capital. In practice, because Atlantics enable no-collateral borrowing, the purchase of the options can only be performed by Dopex managed contracts to ensure that collateral is returned to the option writer at expiry. Dopex currently leverages Atlantic puts to create long straddles by using the put writer’s stablecoin collateral to purchase the underlying, generating the same exposure as a traditional long straddle combination of buying both an ATM call and an ATM put. Atlantics will also facilitate composability with other protocols—Dopex is set to release a perp protection mechanism in collaboration with GMX, a perp exchange on Arbitrum. For a deep dive into Atlantics and the possible application areas, I recommend having a look at this article.

Continuing with composability, Ribbon is building a robust DeFi ecosystem by reinforcing its DOVs through an under-collateralised lending platform and a CLOB options exchange called Aevo. The exchange is built on a custom EVM-rollup and is said to grant access to hundreds of instruments that can be traded across a wide range of strikes and expiries with deep liquidity. The long-term plan is for Aevo to be integrated with Ribbon’s DOVs as the venue where the sold option contracts settle, which is a highly synergistic solution. Firstly, the buyer universe expands and pricing becomes more effective, which solves the misalignment of incentives that was discussed earlier. Secondly, Ribbon naturally introduces consistent flow to Aevo, and more sophisticated DOVs can be built on top of the exchange. Thirdly, vault depositors’ positions could be made liquid by allowing them to trade on Aevo. Then, depositors could take profit or cut losses before expiration, massively increasing the flexibility of Ribbon DOVs. Lastly, Aevo would create liquidity for market makers that currently buy DOV options off-chain, and they could hedge their positions directly on the exchange. Aevo could also be synergistic for other DOV protocols by functioning as an infrastructure layer.

Moving past current solutions

To summarise what has been established in this write-up so far, on-chain option trading is currently facilitated through two mechanisms: CLOBs and option AMMs, both of which have their downsides that require further development to attract wide-spread adoption and deep liquidity. Before blockchain technology progresses further, it’s difficult to argue that on-chain CLOBs will become a viable substitution for CEXs. Furthermore, CLOB-based protocols will have to face additional direct competition in the near term, with projects such as Strike.trade launching soon. The exchange is promised to aggregate fragmented altcoin option liquidity, which traditional CLOB exchanges are structurally incapable of supporting in their current forms, through an electronic request for quote system, where traders request a quote from a set of dedicated market makers.

As mentioned earlier, it’s hard for AMMs to price options correctly because many non-trivial variables have to be considered, and traditional option pricing equations utilised by AMMs rely on several assumptions that certainly don’t hold for crypto assets. To solve the pricing problem, AMMs resort to increasingly complicated equations and compensation mechanisms, which may solve one problem, but usually introduce another one.

Consequently, projects have started experimenting with new peer-to-pool solutions. A promising development in the options space are derivative protocols that are building on top of spot AMM liquidity pools. The idea is to utilise liquidity provider tokens (“LPTs”), which generate a payoff that is mathematically identical to selling a put option. Using LPTs, protocols can build a vast array of payoff profiles by e.g., supplying liquidity to a spot AMM at specific intervals or repackaging LPT returns and splitting them between traders with differing market views. This is the sector I find the most interesting because the implementation enables completely new products that can’t be replicated in TradFi, while solving the problem of convoluted pricing mechanisms utilised by option AMMs.

One of the first protocols to construct option-like payoffs out of LPTs was Primitive. However, unlike most projects today which build on top of Uniswap’s v3 pools, Primitive employed replicating market makers (“RMM-01s”). A RMM-01 was designed such that its LPTs reproduced a covered call payoff, while the underlying assets in the pool could be swapped on a concentrated liquidity curve. Unfortunately, these pools never saw a lot of usage and due to a math approximation error in the RMM-01 design, Primitive shut them down. The Primitive team is now working on solutions for AMM liquidity discovery.

Panoptic is one of the most promising option projects that is building on top of Uniswap v3 LPTs. The three main protocol participants are: 1) LPs that provide capital to Panoptic and earn a yield from their assets being lent; 2) option writers that borrow the capital against collateral and deploy it into Uniswap v3 pools; and 3) option buyers that deposit collateral to cover the potential premiums to the sellers and remove the capital deployed by option writers, which gets relocated back to a Panoptic pool.

Simply put, a short option position is created when capital is deployed to a Uniswap pool, and a long option position is created when the same capital is removed by another Panoptic trader. When an option writer deposits the base asset to a spot AMM, a call option on the base asset is created, while a put option on the base asset is created when the quote asset is deposited. An option’s strike price is generated by locking in a swap rate between two assets in a spot AMM—if an option is ITM, the option holder can swap assets at the defined strike such that they are buying/selling the base asset at a favourable price. A Panoptic option can be bought on any asset that has a Uniswap v3 liquidity pool at any strike price, as long as the specific option has been sold by somebody first.

The price of an option created through the protocol doesn’t decay over time, instead, the price is path-dependent and will grow at each block according to the proximity of the spot price to the strike price. In addition to the traditional option parameters, sellers define the width of an option, which is comparable to providing concentrated liquidity on Uniswap v3. When the underlying’s spot price is in an option’s width, the option writer earns premiums from the buyer. Compared to option AMMs, selling an option on Panoptic isn’t as straightforward because a) underwriters are optimising across a wider set of parameters and b) approximating the premiums from selling is tougher. Thus, sellers have to be sophisticated in order to consistently make a profit, and it’s likely that Panoptic will require professional market makers to create a liquid underwriting market. For an in-depth explanation of how LPTs can be utilised to create options and how Panoptic functions, I recommend reading their whitepaper.

Lastly, options aren’t the only derivatives that can be created by building on top of spot AMM LPTs, and the mechanism could very well become the next DeFi narrative since it serves a purpose for both sophisticated traders who can use the protocols to hedge risk in ways that weren’t possible before, and for degens who want to take on a vast amount of risk. For example, Gammaswap will enable traders to go long and short volatility (gamma) by building on top of Uniswap v3 LPTs. The party that is long gamma will receive returns when impairment losses in the underlying spot AMM increase, while the party that is short gamma gets a yield based on an interest rate that the long gamma party pays for the open position and fees created in the underlying spot AMM. A detailed description of the theory behind Gammaswap and how the protocol works can be found here.

Looking ahead

At the moment, options TVL is oriented towards DOVs. That is, a notable share of liquidity is used for selling options rather than buying them. The structural liquidity mismatch is likely to even out in the future as more and more alternatives for generating yield through options are brought to the market and the space institutionalises, increasing the number of professional market makers providing capital and arbitraging LP returns. Consequently, as competition for yield increases, returns will decrease and capital will flow elsewhere as unsophisticated liquidity provision, on average, becomes less profitable. Balanced capital allocation between buying and selling will be beneficial for the options market since it strengthens price discovery, and most DOVs will likely have to revamp their business models to continue attracting funds.

Unlike when AMMs were implemented for on-chain spot trading, there hasn’t been a clear winning solution in the options space so far. All of the currently used mechanisms carry some form of inefficiencies, while completely new methods that are designed to naturally solve these inefficiencies are yet to be proven. It will be interesting to see if any of the new solutions obtain meaningful market share from mature protocols.

Whichever solution ends up being standardised, the DeFi options space is certain to vastly expand in the medium term. If options in crypto were to reach similar relative usage as in TradFi, on-chain notional options volume would grow by ~60x, even if the penetration of DeFi options stayed flat. However, better technology and infrastructure will enable an increasing number of institutional traders to move on-chain, more products and deeper liquidity, as well as facilitate composability, which will drive up the penetration. When on-chain options can reliably be used as a risk management tool across crypto, adoption will come naturally as more and more protocols start integrating options, and the complexity of the space will increase at a fast pace. As further interdependencies are created and more exotic options are introduced, it’s important to remember that risk never vanishes into thin air, it’s merely transferred.

Hopefully this write-up provided some new information regarding the DeFi options space. All comments and discussions are more than welcome. And as always—thanks for reading! Follow me on Twitter @0x___Brick for more crypto shenanigans and share this article all over, it would mean the world to me!

Well written